Europe’s utilities are at a crossroads. Coal phaseouts, regulatory pressure, and ambitious EU climate targets are reshaping the sector. Using Asset Impact’s physical asset-based datasets, this analysis looks at how three major players—Germany’s RWE, Spain’s Iberdrola, and Finland’s Fortum—are shifting their emissions and energy mix, and how these track International Energy Agency pathways and sectoral benchmarks.

RWE

RWE is a leading global power generation company, headquartered in Germany, with operations across Europe, Asia-Pacific, and the US. The company’s annual forecasted emissions decline by almost a quarter between 2024 and 2030, from approximately 65 MtCO₂e to just below 50 MtCO₂e. The pace of decline, however, remains much slower than that required to be aligned with the IEA’s Net Zero Emissions (NZE) trajectory.

By 2030, RWE remains well above the overall sector benchmark – which compares RWE’s emissions to a normalised global average for the power sector, based on aggregated asset-level data. It serves as a comparative baseline to evaluate whether an individual company is decarbonizing faster, slower, or in line with the wider industry.

While RWE eliminates some of its coal-fired emissions, 14% of installed capacity in 2029 is still fossil-fuelled, placing the company on track for the least ambitious IEA pathway – the 1.7–2.4 °C Stated Policies Scenario (STEPS) – and well above the 1.5C-aligned NZE pathway.

This gap reflects structural inertia in the company’s transition plan implementation: while RWE makes some progress in reducing absolute emissions, it does not do so fast enough to fully align with climate-safe pathways.

According to Asset Impact’s forecasts:

- Renewables rise to 53% of total capacity by 2029, a substantial improvement from 37% in 2022. However impressive this may seem, the lower utilization rate of renewable resources means this will still represent a minority of electricity generated.

- Renewables rise to 53% of total capacity by 2029, a substantial improvement from 37% in 2022. However impressive this may seem, the lower utilization rate of renewable resources means this will still represent a minority of electricity generated.

- Coal capacity declines from 24% to 14%, a clear positive signal for long-term alignment, but still short of the 11% NZE target for 2029. It is worth noting that the NZE target is a global average, and as a technologically advanced German utility, in practice RWE should be expected to outperform the global benchmark and achieve deeper reductions in order for the books to balance at a global level.

- Gas capacity remains unchanged at 29%, significantly above the IEA NZE global trajectory of 18% for 2029.

This continued reliance on fossil fuels keeps RWE’s Implied Temperature Rise (ITR) above the 1.5°C pathway. While the utility is directionally aligned with decarbonization, the composition of its energy portfolio, particularly its gas-fired capacity, suggests that it may be locked into medium-term fossil fuel use, with potential exposure to future regulatory tightening. Its renewable portfolio growth, while significant, is not enough to achieve an NZE-aligned decarbonisation rate.

RWE’s asset-based transition trajectory gives us mixed signals. On one hand, its rapidly growing renewables portfolio and progressive retirement of coal indicates solid progress in the right direction. On the other hand, gas still comprises a third of installed capacity at the end of the decade. Along with a shrinking but persistent attachment to coal, this suggests RWE’s investors and creditors should not dismiss the transition risks sitting stubbornly within its power generation portfolio.

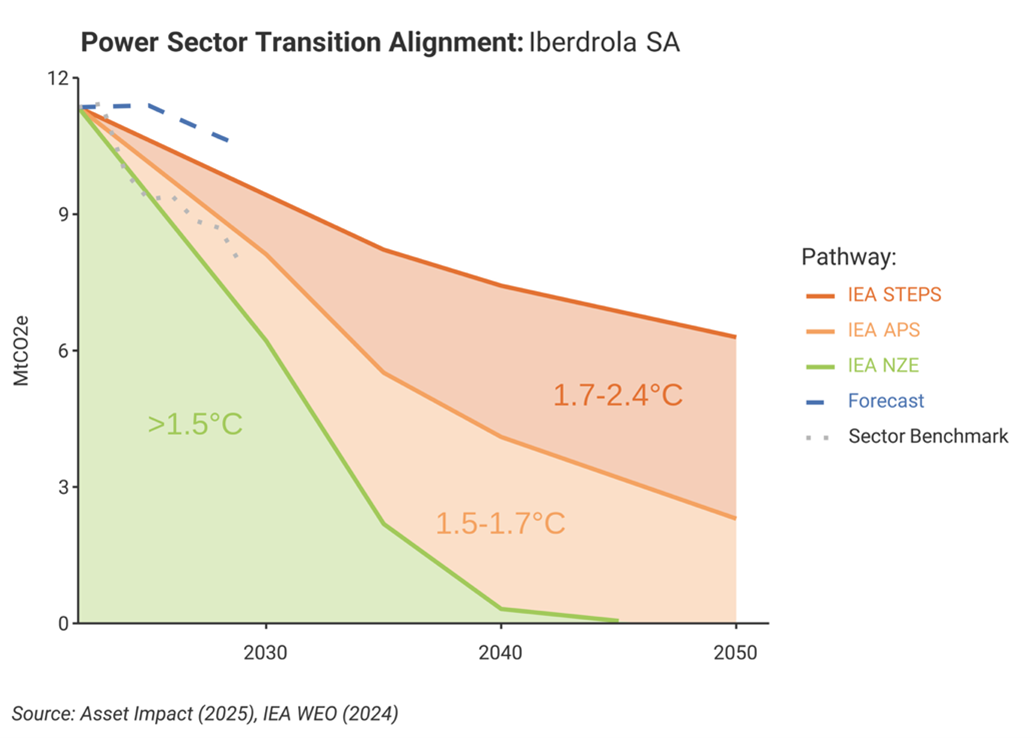

Iberdrola

Iberdrola has long been regarded as a European renewable frontrunner. Its low baseline emissions (~11.4 MtCO₂e in 2024) support this perception. But Asset Impact’s forward-looking data shows a flattening decarbonisation trajectory, with emissions barely declining below 10 MtCO₂e by 2030.

The composition of Iberdrola’s mix reflects a mature portfolio, but a static one. It has been coal-free since 2020, and its hydro-heavy base, supplemented by nuclear and almost 50% renewables by capacity keep emissions significantly lower than peers. But without meaningful change in gas-fired capacity, the company’s emissions plateau, undermining long-term alignment.

Thus, despite its deserved reputation as a green leader, under the ITR methodology, Iberdrola does not align with the IEA NZE pathway. Its emissions fall above the 1.7–2.4 °C range, outperforming peers like RWE in absolute terms but failing to demonstrate momentum in reducing emissions further. This highlights the fact that, having a lower total emission number than peers does not mean the company is necessarily doing enough to align with ambitious pathways.

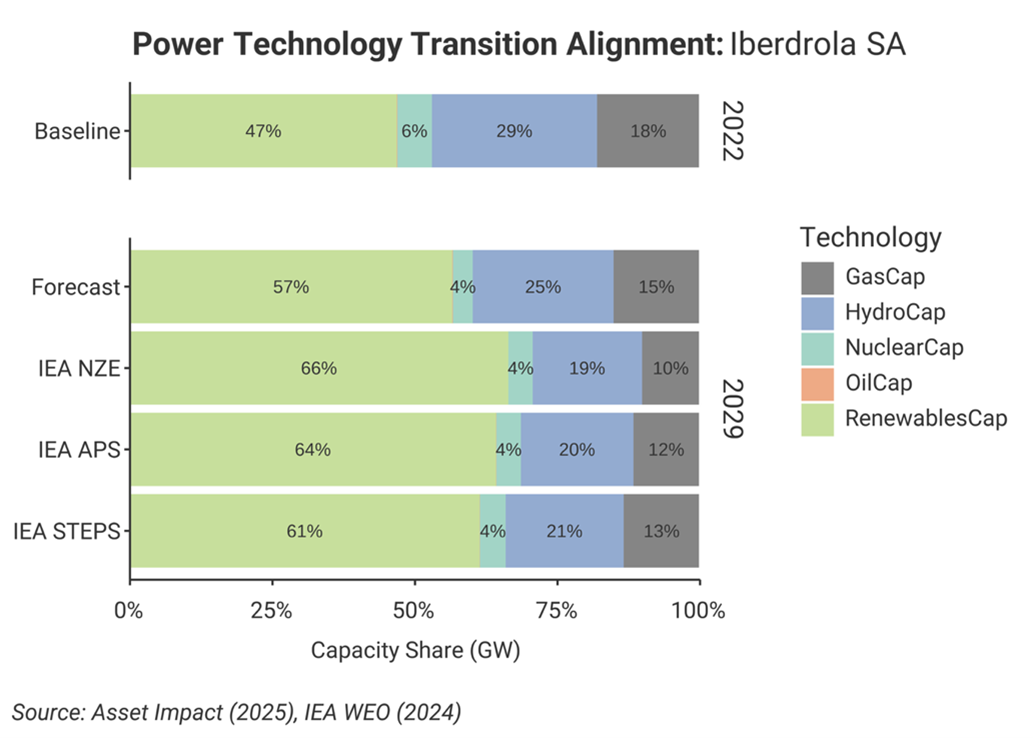

In terms of installed capacity:

- Renewables as a share of total capacity will increase from 47% to 57% by 2029, a strong performance relative to peers, but below any IEA expectations given Iberdrola’s already high baseline.

- Hydropower stays relatively steady at roughly one quarter of Iberdrola’s capacity mix.

- Gas remains stable at ~15% and does not diminish significantly, while oil and nuclear remain marginal.

While Iberdrola leads from the front in its deployment of renewable capacity, its additional emissions reductions up to 2030 remain shallow due to steady gas and coal. The company’s profile suggests strong green credentials but highlights the difficulty of the remaining decarbonization challenge ahead.

For stakeholders, the key question is whether Iberdrola can accelerate its emissions reductions. Without a steeper downward trajectory, its Implied Temperature Rise (ITR) is likely to remain above levels consistent with the IEA benchmarks.

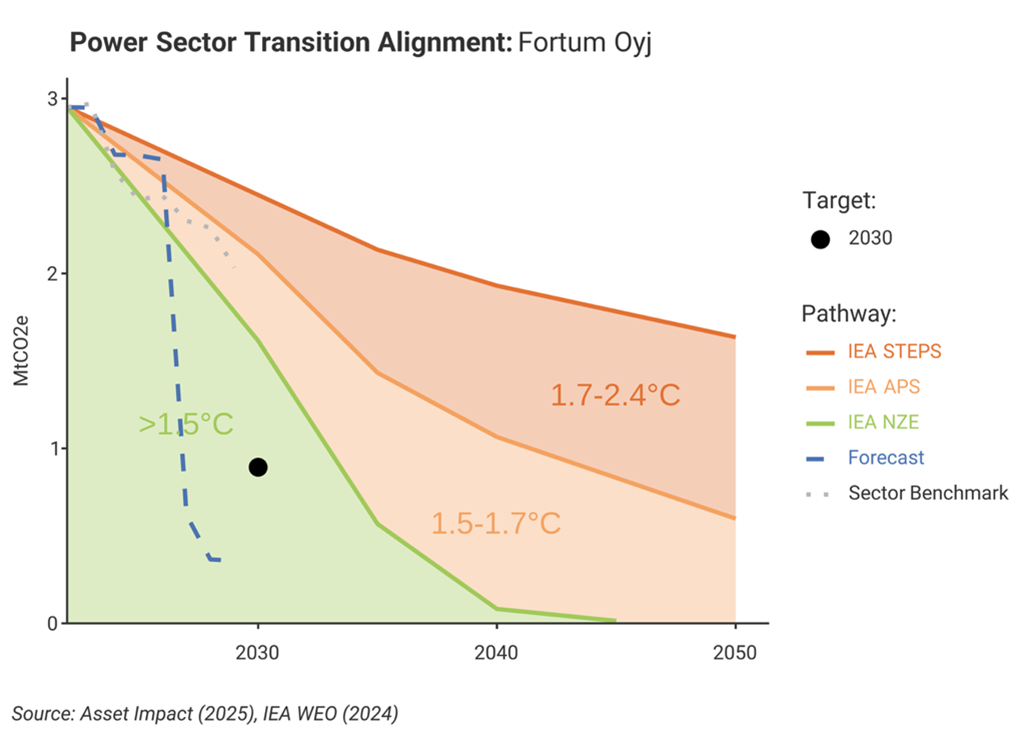

Fortum

Among the three utilities, Fortum shows the most rapid drop in forecasted emissions. Asset Impact’s models suggest a decline from ~3 MtCO₂e in 2024 to below 1 MtCO₂e by 2030, outperforming the IEA NZE trajectory given its relatively high baseline. As a result, Fortum’s implied temperature rise falls below 1.5 °C, placing it in rare company among European utilities.

However, this sharp decline favouring Fortum’s success in emissions reduction is largely a result of shifts in its legacy hydro and nuclear portfolio, rather than transformative investment in new renewables or early gas retirements.

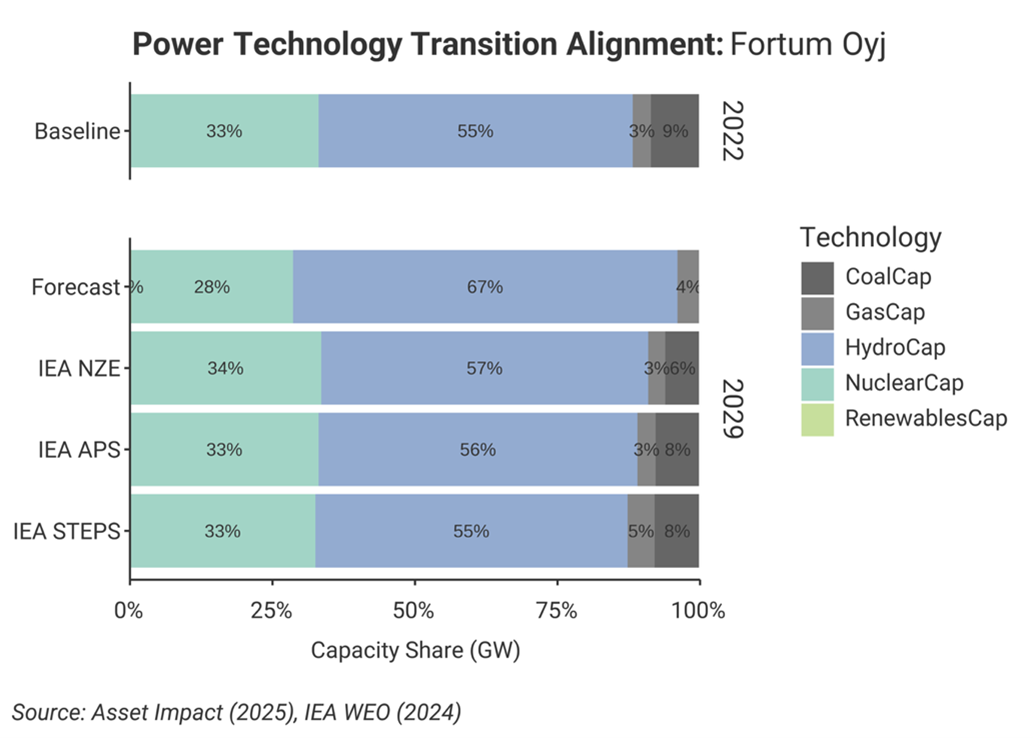

Looking at forecasted changes in Fortum’s capacity mix shows that:

- Hydro will continued to provide two-thirds of Fortum’s capacity, making it a cornerstone of the company’s alignment planning.

- Other renewables (including solar and wind) remain completely marginal.

- Gas still represents 4% of the portfolio, a marginal increase from 3% in 2022, although coal is expected to be completely phased out from 9% in 2022 to zero in 2030.

Unlike RWE and Iberdrola, which are actively replacing coal or gas with wind and solar, Fortum appears to be relying on the stability of low-emission hydro and nuclear assets. That strategy is enough to make Fortum aligned in 2030, but won’t be sufficient to keep it in the NZE alignment range in 2040 without the removal of its remaining gas assets.

Conclusion

Asset Impact’s granular, asset-based data shows how when it comes to assessing the credibility and dynamics of company transition plans, the devil is very much in the detail. Comparing three leading utilities, we find:

- RWE, one of the bedrocks of the German utility sector, is making significant emissions cuts but is held back by its continued dependence on gas and coal for over 40% of installed capacity in 2030.

- Iberdrola, a leading renewable player headquartered in Spain, has made significant progress to date, but its emissions reduction rate is at risk of stalling as, like RWE, it grapples with a persistent gas problem.

- Finnish utility Fortum expects to gradually expand its extensive large-scale hydro assets to replace declining nuclear and coal capacity, which is sufficient to ensure rapid alignment, though with limited renewables growth and some gas still remaining by 2030.

Together, these cases illustrate how uneven the EU power sector transition remains when comparing companies’ trajectories to 2030 against a common baseline. For banks lending to these firms, these asset-based insights can help to pinpoint where companies truly are aligning, and where transition risks still loom.

Let's talk

Looking for more details on using our forward-looking asset-based data? Our team is here to support you.

Contact us